Retirement Options for Exempt Employees

TCRS Hybrid Retirement Plan

The Hybrid Retirement Plan is comprised of two valuable components: a defined benefit plan provided by the Tennessee Consolidated Retirement System (TCRS) and a 401(k) plan offered through Empower Retirement.

Your defined benefit plan - Tennessee Consolidated Retirement System (TCRS)

Recognized as one of the top performing defined benefit plans in the country, TCRS provides lifetime retirement, survivor and disability benefits for employees and their beneficiaries. After a five-year vesting period, an employee becomes eligible to receive a monthly benefit at retirement once the age requirement is met. The benefit is calculated by the employee’s years of service and salary. The benefit provided by TCRS is a solid foundation for building a retirement future.

Your 401(k)

The 401(k) plan lets you take control of your retirement by investing in fund options of your choice. You are immediately vested in the 401(k) and can decide how your money should be invested given your individual goals, risk tolerance, and timeline. The amount you receive from your 401(k) account in retirement is based on how much you save, plus any accumulated earnings from your investments.

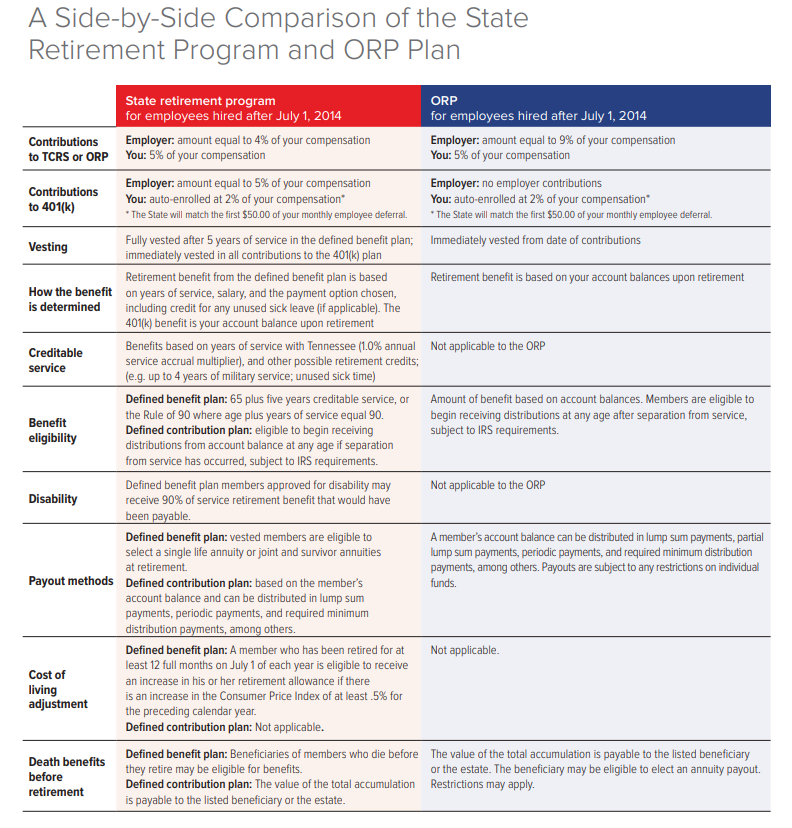

Hybrid plan (for employees hired on or after July 1, 2014)

Your retirement is funded by contributions from both the State of Tennessee and you, the member. The State makes a contribution equal to 4% of your salary into TCRS and 5% into your 401(k). You, the member, contribute 5% to TCRS and 2% to the 401(k) plan. Your contributions to the 401(k) plan may be made on a pre-tax or after tax (Roth) basis, meaning you can choose whether the money will be taxed now or in retirement. The State of Tennessee provides a retirement plan that gives you an excellent start toward a successful financial future.

| Contributions to your Hybrid Retirement Plan | |||

|---|---|---|---|

| Employer contributions | Member contributions | Total contributions | |

| TCRS | 4% | 5% | 9% |

| 401(k) | 5% | 2% | 7% |

| TOTAL | 9% | 7% | 16% |

Your member contributions to the 401(k) qualify for a $1 match for every $1 contributed to the State of Tennessee 401(k) plan each month, up to $50, for the fiscal year beginning July 1, 2024, and ending June 30, 2025. That’s a maximum match of $50 per month for contributions of $50 or more! Log into your 401(k) account now at RetireReadyTN.gov.

Learn more about the Hybrid Plan.

Legacy plan (for members hired before July 1, 2014)

Members hired prior to July 1, 2014, are in the Legacy Plan, and are non-contributory to their defined benefit (TCRS) plan. Members can also participate in the 401(k) and 457 plans. Your member contributions to the 401(k) plan may be made on a pre-tax or after tax (Roth) basis, meaning you can choose whether the money will be taxed now or in retirement. Your member contributions up to $50 to the 401(k) also qualify for a monthly $1 match for every $1 contributed.

Learn more about the Legacy Plan.

To schedule a Retirement Counseling session as a TCRS member, please call the RetireReadyTN call center at (800) 922-7772.

Optional Retirement Program (ORP)

The ORP is a defined contribution plan that lets you take control of your retirement by contributing to investment options of your choice. You are immediately vested in the ORP and can decide how your money should be invested given your individual goals, risk tolerance, and timeline. The amount you receive from your ORP account in retirement is based on the value of your account at the time of distribution.

The ORP is offered through two plan providers – TIAA and Voya. More information about their specific investment options can be found at the links below:

Or you can contact our ORP representatives:

|

TIAA-CREF |

Rosaline Rogers Banks, CFP, CRPC |

|

VOYA |

Michael V. Biggs, ChFC, CLU, MBA michael.biggs@equitable.com

1817A Madison Street | Suite 3 |

Exempt faculty and staff hired after July 1, 2014, are eligible to participate in the Hybrid ORP Plan. Hybrid ORP members are automatically enrolled in the state’s 401k plan at 2% of salary. Learn more about the Hybrid Plan.

Exempt faculty and staff who were ORP members prior to July 1, 2014 are in the Legacy ORP Plan. The Legacy ORP plan is closed to new enrollees. Learn more about the Legacy Plan.

Additional information about the Hybrid and Legacy ORP plans can be found at RetireReadyTN.

| Contributions to your ORP | |||

| Employer contributions | Member contributions | Total contributions | |

| ORP | 9% | 5% | 14% |

| 401(k) | 0% | 2% | 2% |

| TOTAL | 9% | 7% | 16% |

Your member contributions to the 401(k) qualify for a $1 match for every $1 contributed to the State of Tennessee 401(k) plan each month, up to $50, for the fiscal year beginning July 1, 2024, and ending June 30, 2025. That’s a maximum match of $50 per month for contributions of $50 or more! Log into your 401(k) account now at RetireReadyTN.gov.

What is a 401(k) plan? A 401(k) plan is a retirement savings plan designed to allow eligible employees to supplement any existing retirement and pension benefits by saving and investing your taxadvantaged dollars through voluntary salary deferral. You may select from pre-tax and after-tax (Roth 401(k)) deferral options. Pre-tax contributions and any earnings on contributions are tax-deferred until money is withdrawn. Distributions are usually taken during retirement, when many participants are typically receiving less income and may be in a lower income tax bracket than while working. Distributions from pre-tax contributions are subject to ordinary income tax. If taken before you reach age 59½, distributions may be subject to an additional 10% federal early withdrawal tax.

What is a Roth 401(k) contribution? A Roth 401(k) contribution is an option under the 401(k) plan that allows eligible employees to supplement any existing retirement and pension benefits by saving and investing after-tax dollars through voluntary salary deferral. Contributions and any potential earnings can be distributed on a tax-free basis after you have reached age 59½ and after the required five-year holding period has passed. You have to designate all or a portion of your 401(k) elective deferrals as Roth contributions.

Log into your 401(k) account now at RetireReadyTN.gov.

The 2024 maximum contribution limit is $23,000. The catch-up contribution is an additional $7,500. This maximum contribution limit is an aggregate total of the 401(k) and 403(b).

What is a 457 deferred compensation plan? A governmental 457(b) deferred compensation plan (457 plan1 ) is a retirement savings plan that allows eligible employees to supplement any existing retirement and pension benefits by saving and investing pre-tax dollars through a voluntary salary contribution. Contributions and any earnings on contributions are tax deferred until money is withdrawn. Distributions are usually taken during retirement, when many participants typically receive less income and may be in a lower income tax bracket than while working. Distributions are subject to ordinary income tax. The early withdrawal penalty does not apply to 457 plan withdrawals. The 457 deferred compensation plan does not offer a Roth option.

Log into your 457(b) account now at RetireReadyTN.gov.

The 2024 maximum contribution limit is $23,000. The catch-up contribution is an additional $7,500.

What is a 403(b) plan? The 401(k) and 403(b) are very similar in design. Both are deferred compensation plans with immediate vesting. The main difference is the financial institutions that participate in the plans. Empower is the only provider in the 401(k), whereas the 403(b) has two ORP providers. Therefore, an employee could elect to contribute supplemental/voluntary funds to the same financial institution that they selected for the ORP, should they participate in ORP.

To make changes to your 403(b) account, complete a 403(b) contribution form or 403(b) termination form and return it to the Benefits office.

The 2024 maximum contribution limit is $23,000. The catch-up contribution is an additional

$7,500. This maximum contribution limit is an aggregate total of the 401(k) and 403(b).

A chart displaying the differences between the 403(b) and 401(k) is below:

|

|

403(b) |

401(k) |

|

Providers |

TIAA & VOYA |

Empower |

|

Eligibility |

All active higher education employees |

All active state employees |

|

Contribution Source |

Employee deferrals |

Employer and Employee deferrals |

|

Investments |

Investments are self-directed |

Investments are self-directed |

|

Distribution Options |

Based on the individual’s account balance. Individuals are eligible to select: single life annuity, joint and survivor annuity, lump sum payments, periodic payments, and required minimum distribution payments, among others |

Based on the individual’s account balance. Individuals are eligible to select: lump sum payments, periodic payments, and required minimum distribution payments, among others |

|

Vesting |

100% immediate |

100% immediate |